So I don’t actually know yet how we are going to pay for our project. I know, right? The trick is that if you haven’t done it before and just “know”, you don’t really know until you have a designed and appraised project. This is what the many lenders/brokers I talked with asked: do you have a design? Do you have an appraisal? Well, no, I was hoping to get some answers before we committed. But it seems to be one of those things we will only really learn by doing and bumbling through.

Here’s what I do know, and the basis for my high level confidence that our project makes financial sense:

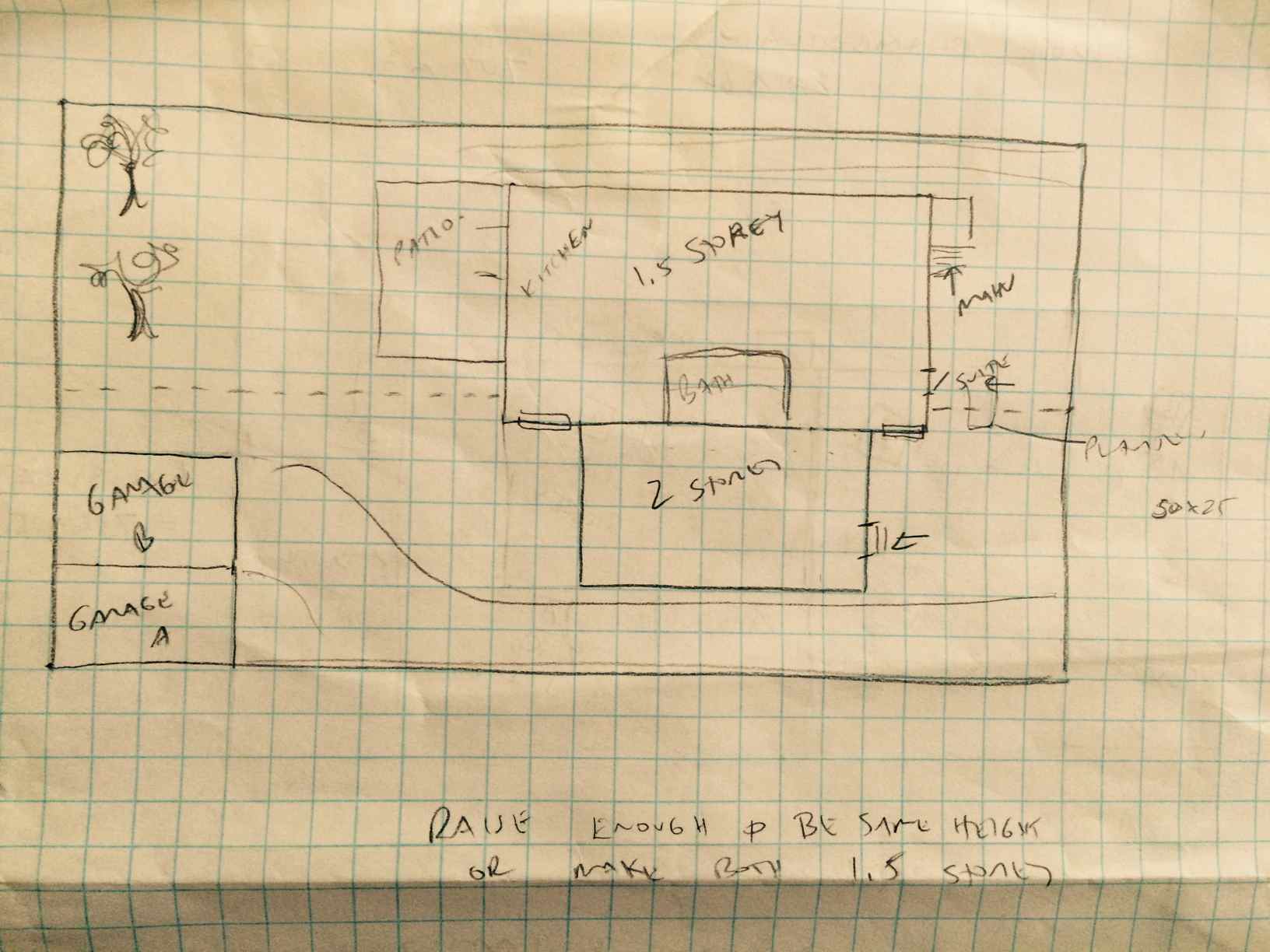

We bought the house for $565,000. We can build the attached or detached new house for $300,000-$400,000, and we can renovate the existing house for around $200,000. If we built an attached addition, we could sell it for $500,000 – $600,000, which covers the cost of the new build and the renovation. We are then left with a renovated house with a suite for the same cost as the original house, but with the added rental income. So overall, our project makes financial sense. If we go the detached route, the construction cost numbers don’t really change, but the sales price is likely closer to $700,000.

But wait! There’s a piece in between: regardless of how good the end picture looks, a lender is not going to lend based on future potential alone. And! The lending scenario looks different if we go with the attached/strata option versus subdividing and building a separate dwelling on its own titled lot.

Here’s what I learned from our mortgage broker Scott Travelbea, who did his own lot subdivision development project a couple of years ago:

For both the subdivision and attached dwelling options, we need to self fund the project to the point where we have approval for the subdivision/rezoning and/or development permit application. However, for the subdivision option, once we have that new lot serviced and titled, it now has real value to a lender, and they are willing to lend against that serviced lot. If the project fails, they have something of value that they can turn around and sell to recover their costs.

In order to be approved for a loan on top of our existing mortgage, we also need to have 20% equity in the existing house, and some money to get the construction started.

In an attached duplex/strata scenario, we need to be much further along in the construction before a lender will be comfortable throwing money at us. If we screw up the project and don’t finish, there isn’t much of value for the lender to recover, given shared land, shared walls etc.

So let’s look at our numbers for the detached option:

- We have $80,000 down on the existing house on a purchase price of $565,000 (14%).

- We currently have $100,000 and change in the bank to fund the rest of the project.

- Say we can limit upfront design and rezoning application costs to $20,000.

- Once the project is approved, both houses will be re-appraised and we may need to put in some extra cash to bump us up to 20% equity in the existing house – let’s assume another $30,000 (based on the purchase price).

- Then we need some cash to get us through to the first construction phase draw – if $50,000 is enough to get started here, we are in business.

My current feeling is that if we do, in fact, have enough money now, we barely have enough money now.

The downside to doing a detached option is that we do not get the additional passive benefit of the combined building volume (minimizing our exterior surface area to internal volume ratio). However, we can sell a detached house for more than an attached strata duplex, at roughly the same cost to build. The detached option is easier to manage long-term since there is no common property. We may not meet Passive House standard, but ultra low energy/net zero is still feasible with a simple smart design and a good enclosure.