Site walk with our “team” soon after conditions were removed

The house sat on the market for 6 months last year and I didn’t see the listing because it was out of our listing price range at the time ($600,000 or less). It was re-listed this year at $599,000 and got no early bites. I barely noticed it the first time I saw it, but eventually circled back. I found that I only saw the houses with good curb appeal the first time around, so I would later comb through older listings to see if I’d missed something with potential. This was one of those properties.

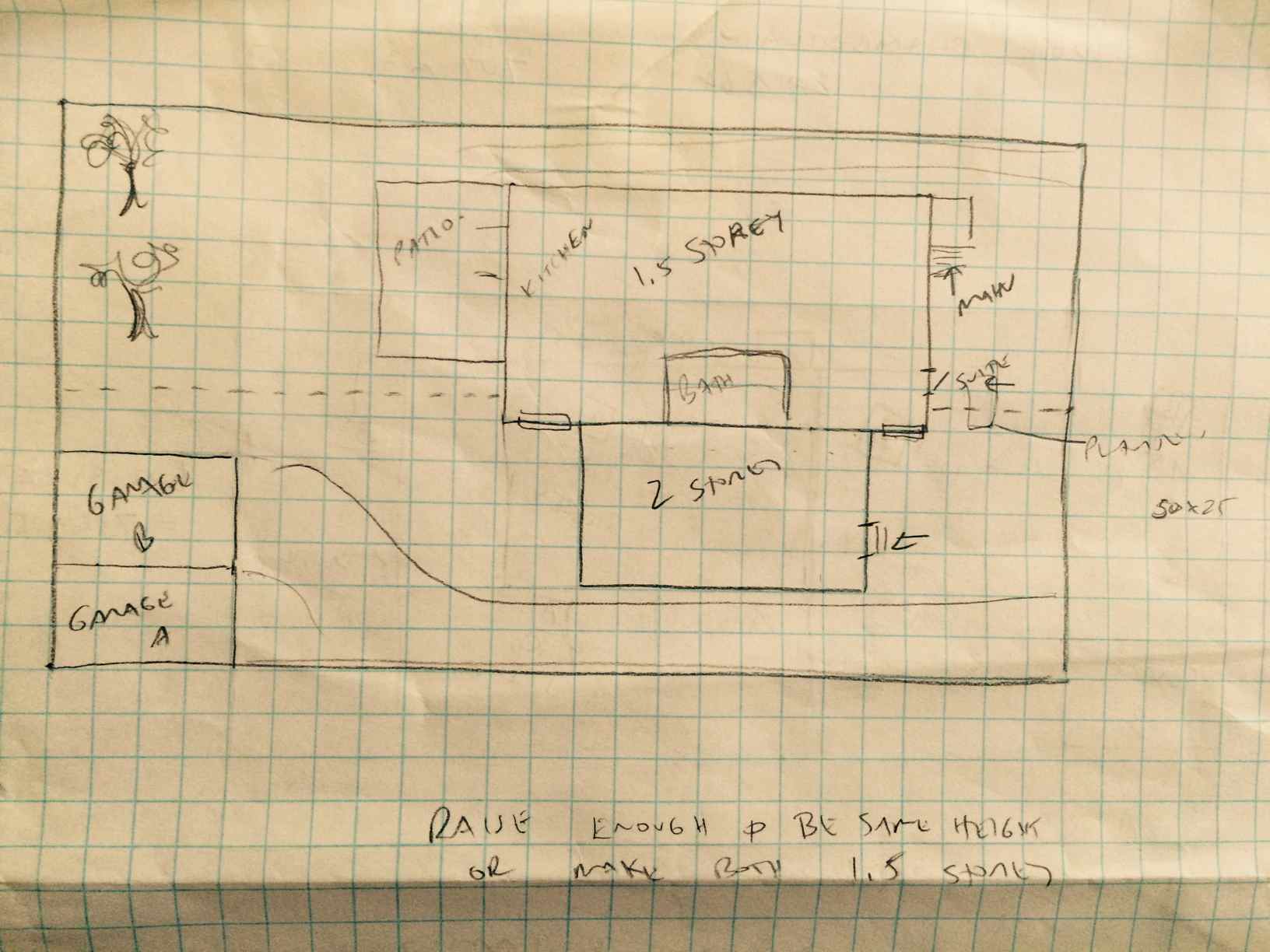

We visited the property in late March 2015. It was a stinky smoker house that was old but with good bones, reasonably cared for and livable. It had a low 6’ basement with a finished room and bathroom added, which was laughably called the “master suite” in the listing- so long as this “master” is 5′ tall with no sense of smell. The location was great and the lot big (~7600 sqft /700 sm).

At this time, though, my American Matt had only just received his Canadian permanent residency and had started working 2 days a week. We couldn’t afford anything near $599,000, which we felt was overpriced anyway. So we tried a low-ball offer at about the land value: $500,000. They countered by dropping the price to $595,000. Ha! I talked to our lender – what was the most we could afford? $540,000 if we really stretched it. OK, let’s try that. No dice. They still wanted more and the offer died.

I kept thinking about the property. I drew more sketches, crunched more numbers, and felt more convinced that this was a good one.

Meanwhile, the house had now been on the market for 30 days, which is an eternity for a house in this location and in this market. It was clearly overpriced. I thought about approaching the owners without an agent as a way to lower the sales price with less impact on the funds going to the sellers. Ultimately, I wasn’t confident enough about how to write an offer to go this route.

A couple of weeks later, they dropped the price to $575,000 and they suddenly generated a bunch of interest. At the same time, Matt had picked up another day of work and was approaching the end of his 3 month probationary period (typically a requirement of the lender). They would be accepting offers until 5PM the next day. I ran the numbers with our mortgage broker again using Matt’s new income. We could now purchase up to $580,000 with $80,000 down and an uncomfortably high monthly payment.

We took another shot: $551,000, and made it only subject to financing but not inspection in an attempt to sweeten our offer. We were one of three offers and they accepted the highest, at $565,000. Lost it again, and this time it hurt a little more. I counseled myself that if it was meant to be, it would be. There is always another house! But I was still bummed. We found ourselves wondering – if the numbers and the project and the location all look so good, would it have been worth the extra $15,000 up front to get the damned thing?

6 days later, our agent Christina called us to say the other deal fell through and would we like to put in another offer (this would be our fourth kick at the can!)? Ok! Let’s do this! We offered $560,000, same conditions as last time. They had also reached out to the other buyers who had lost out on the last round, so again they had multiple offers to consider. They came back to us and said that the other party offered $565,000 but they liked our conditions better, so if we could match their price, the house was ours. So we went for it. The extra money spent did not mean our project would no longer be viable, so it seemed silly to pass this one up. And with four chances, it was clearly meant to be!

After some hiccups around Matt’s employment history in Canada, the conditions were removed on May 8, 2015 with a closing date of July 2. Phew.